Balance Sheet - Free Excel Download

Financial Statements - The Balance Sheet

You as manager need to fully understand your role in the budgetary process. It is the most basic financial planning and control tool. Every manager needs to know what costs are associated with their department, and how in relation are they doing to that budget. You might achieve your departmental goals, but if you go over budget in order to achieve those goals, you create financial problems for the company and jeopardize your own job performance review. In most cases, part of your performance appraisal will be based on whether or not you were within budget for the year.

Budgets need to be realistic. You can’t just say at a whim you need 20 new people, just as upper management can’t say you have only $10 for a years worth of training classes. Budgets are used to investigate variances, whether you went over or under budget, and address the reasons for the variances. You need to always look at ways to control those variances by controlling costs. By being on top of your budget, you might be able to make changes before it’s too late and you end up having to reduce staff or eliminate a branch of your department.

Great managers always look at significant expenses they can reduce or eliminate, such as overtime, travel and entertainment. Also keep in mind, just because you created a budget for the year, it can change if sales are bad or below target. You might have the budget to hire someone, but it can be eliminated if sales do not improve, thus a hiring freeze. You might also have an employee who quits and you cannot replace them, which is known as attrition. You will during your managerial career have to deal with ways of cutting costs, including layoffs. On the other hand you might be able to increase your previously budgeted staff if sales are better than expected.

There are basically two types of budgets, a capital expenditure budget and operating budget:

- Capital expenditure (also known as “Capex”) relates to costs associated with plant and equipment. This is equipment that generally lasts for more than a year such as a copy machine.

- Operating budget, which is related to the normal day-to-day operations and expenditures such as payroll, supplies, and miscellaneous. There are two types of budgets within an operating budget, sales budgets and expense budgets:

- Sales budget is associated with comparison and variance of the actual revenue brought with the projected revenue.

- Expense budget applies to all areas incurring operating expenses, including the sales department. This is the budget we will focus on.

Lets look at a budget as if you are the “Customer Service Manager” in which you would mostly work with finance on budgetary items like staffing (payroll), training expenses, software licenses needed, and general expenses. You would need to make sure that you have your staffing goals and needs figured out and stick to them as close as possible. You should really look over the budget carefully with finance; due to sometimes items might be in your bucket that you feel belong to another department. Finances job is to make sure everyone submits their required operational expenses and then compiles those numbers for upper management in a way that makes sense. Finance acts as a middleman between department heads and upper-management when it comes to budgets. It is not their job to decide on what you need. They have been given a monetary amount from upper management and should help you allocate to your needs.

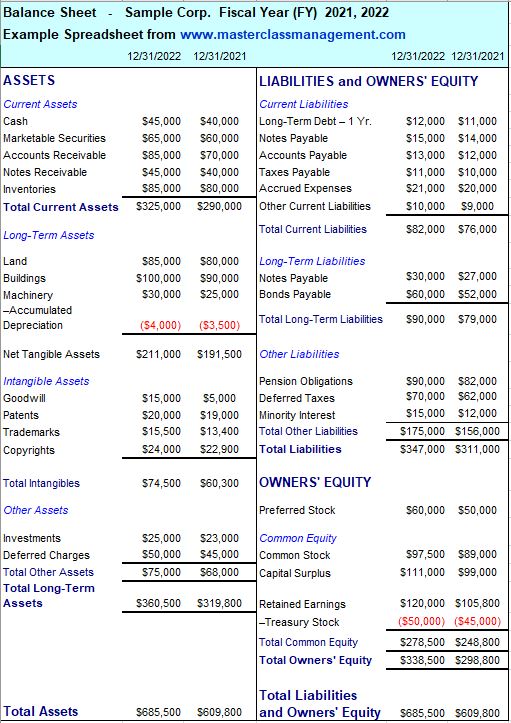

Here is a brief explanation of the type of Assets, Liabilities, and Owners’ Equity associated with a common Balance Sheet:

ASSETS

– which is everything the company owns. They are listed in order of their liquidity, which means how easily they can be converted into cash. Current assets are first, then noncurrent assets, and finally all other assets.

Here are the most common types of assets:

Cash, both in checking and savings along with petty cash.

Marketable Securities, which are short-term investments, like U.S. Government securities or the commercial paper of other firms. These often earn higher interest than checking or savings accounts earn.

Accounts Receivable, which is money owed to the company by its customers, usually within 10 to 60 days. There is usually also some bad debt, around 2%, that gets written off. For example, a customer who purchased your product but never paid.

Notes Receivable, which is money due from debtors.

Inventory, which is the goods for sale to customers, or goods in the manufacturing process.

- The inventory for a Manufacturer would be the raw materials to make its products, the unfinished products still being made, and the finished goods that are awaiting sale.

- The inventory for a Retailer would be just the finished goods. They would not deal with the raw materials or have an unfinished product.

- The inventory for a Service company would have little to no inventory on their balance sheet due to the nature of the business.

Long-Term Assets or Tangibles, also known as “Fixed Assets.” The land, buildings, factories, and warehouses, including the machinery, furniture, computers, and fixtures that are owned by the company. These assets can depreciate, or lose value, on each year’s balance sheet due to age, etc.

- Accumulated depreciation is a way to allocate, which means assigning, the cost of a fixed asset with a life of over one year. The cost of the asset is charged against income over the life of the asset rather than all in one year. This is also known as a “contra account,” which in essence carries a minus sign.

Intangible Assets, which are non-physical products like patents, which are exclusive legal rights granted to an investor for a period of 17 years, trademarks, which are distinctive names or symbols granted for 28 years with option for renewal, goodwill, which is the amount of money paid for the asset above the value it was assigned by the previous owner, and copyrights, which is a form of intellectual property that gives the creator of an original work exclusive rights for a certain time period.

Investments, Prepayments and Deferred Charges, which is monies already spent, that will yield benefits in upcoming years like insurance coverage, rent, etc.

LIABILITIES

– which is everything the company owes, mostly to suppliers and creditors. Current liabilities are those payable within a year of the date of the balance sheet. Here are the most common types of liabilities:

Long-term debt, which is the debt due after one year of the date of the balance sheet.

Notes Payable, which are short-term borrowings that are payable within the year. It is a promissory note, which is basically a written promise to pay.

Accounts Payable, which is the amount the company owes to suppliers.

Federal income taxes, and when applicable city and state taxes.

Accrued Expenses Payable, which is all other monies, owed at the time of creating the balance sheet including employees, contractors, utilities, etc.

I.e. Current portion of long-term debt, which is the amount due within a year from the date of the balance sheet. This would be considered a current liability.

Notes Payable, which are non current (due after 12 months) borrowings. It is a promissory note, which is basically a written promise to pay.

Bonds payable, which is the obligation due on maturity of bonds.

Pension obligations, which is the liability for future pension benefits due to employees.

Deferred Taxes, which are the longer-term tax obligations that have been deferred to some future period.

Minority interest, which is the ownership of minority shareholders in the equity of consolidated subsidiaries.

OWNERS' EQUITY

(also known as Stockholders’ Equity - when applicable) – which is the amount left over for the company’s owners after the liabilities are subtracted from the assets. The formula is “Assets – Liabilities = Owners Equity.” This is also referred to as “Net Worth.” If the company is incorporated, they can issue stock. Stocks represent ownership in a corporation. A share of stock is one unit of ownership. Investors buy stock to share in the company’s profits, where as the company issues stocks to raise money from the investors. If the company is not incorporated, such as a Sole Proprietor, they will not have accounts for stock, but will invest the money back into the company through “Retained Earnings.” If this number is zero or negative, then the company is obviously in trouble and steps will need to be taken, or else there is the chance of bankruptcy.Preferred Stock, which is a type of stock that pays a dividend. It is a payment from profit made to stockholders out of the company’s income at a specific rate, regardless on how the company performs. Owners of preferred stock do not have voting rights such as who should be on the Board of Directors or whether or not to sell the company. They only get dividends if the company has earnings to pay them. It is called preferred because the dividend must be paid before dividends are paid on the common stock.

Common Stock, which the owners have voting rights, but do not receive dividends at a fixed price. The value of the stock can rise or fall.

Capital Surplus, also known as “additional paid-in capital,” is the amount paid to the company in excess of the par value. When a company issues a stock, the stock has a par value, a value assigned to a share of stock by the company. This value does not determine the selling price, or market value, of the stock. The selling price that the investor pays per share is determined in the market.

Retained Earnings, which is money reinvested into the company and becomes part of the capital that finances the company.

Treasury stock, which is stock in the company that has been repurchased and not retired.

As you can see, the “Total Assets” for each year equaled the “Total Liabilities Equity.” It is called a “Balance Sheet” because it has to balance. Each dollar value was a “Snap-Shot” on the date of the financial statement. Assets are in order of their liquidity and how fast they can be converted into cash. Current assets are expected to be liquidated within one year of the date of the Balance Sheet. Liabilities and Equity are in order in which they are to be paid.

Current Liabilities are payable within one year. Also, as you can see, there are two years of figures on the balance sheet for comparison and trending purposes.

| ||||